Biden Effect: 2/3 of the U.S. Population Now Lives Paycheck to Paycheck

- As Rising Inflation Makes Paying Bills and Building Savings Increasingly Difficult, More Consumers of All Income Brackets Join Their Ranks

- Paycheck-to-Paycheck Consumers are Three Times More Likely to Revolve Credit Card Debt and Carry Higher Monthly Balances

A report released Monday examines the growing shares of U.S. consumers in all economic brackets living paycheck to paycheck, and the impact on their ability to access credit and other expense management tools.

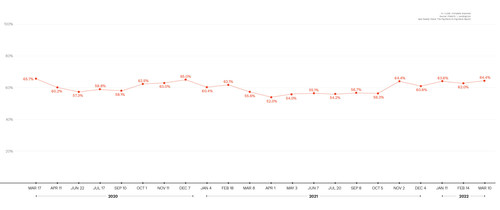

Key takeaway: Living paycheck to paycheck has become the dominant way people manage their cashflow in the United States, with close to two-thirds of the U.S. population, 64% or about 166 million adults, doing so in March 2022.

Living paycheck to paycheck means devoting all of one’s salary to expenses with little to nothing left over at the end of the month, yet many of these consumers remain credit worthy, actively managing their cash flows in real time. In fact, close to one-quarter of consumers living paycheck to paycheck report a credit score higher than the FICO average of 750.

“The number of people living paycheck to paycheck today is reminiscent of the early days of the pandemic and it has become the dominant lifestyle across income brackets,” said Anuj Nayar, Financial Health Officer at LendingClub. “As inflation we have not seen in a generation takes more of our paychecks for everyday needs, Americans across incomes and credit scores are increasingly relying on credit products just to get by. That is why the financial services industry must offer better tools to help bridge the gap.”

A Deeper Look at Credit Scores

PYMNTS’ research finds that paycheck-to-paycheck consumers without issues paying their bills have an about average credit score of 694, while those struggling to pay bills each month have a below average credit score of 613. The average credit score for all paycheck-to-paycheck consumers is 664, more than 90 points below the average for consumers not living paycheck to paycheck. Meanwhile, the gap between the average credit scores of low- and high-income consumers is less than 90 points. Consumers who earn less than $50,000 report a below average credit score of 648, while those earning more than $100,000 report an above average credit score of 734.

The data also finds that consumers who are financially struggling tend to check their credit scores more frequently. Of those consumers who live paycheck to paycheck with issues paying their bills, 20% checked their credit scores in the 24 hours before PYMNTS’ survey compared to only 9% of consumers who live paycheck to paycheck without issues paying their bills.

Credit And Living Paycheck to Paycheck

The report continues to find that credit card ownership remains high, with 63% of respondents of all financial lifestyles saying they have made a credit card payment in the last 90 days.

Paycheck-to-paycheck consumers are three times as likely to revolve credit card debt and carry higher monthly balances overall. Those consumers who never pay their credit balances in full also tend to hold more credit cards than average. PYMNTS’ research finds that 29% of credit card holders “always” or “usually” revolve their balances.

On average, credit card holders have approximately two credit cards, which rises to three credit cards among those not likely to pay their credit card in full (i.e., those who “always” or “usually” have a revolving balance). Moreover, the data finds that the average sum of monthly balances over the last six months for those who always revolve balances on their credit cards is triple the average of those who always pay in full.

Struggling consumers also tend to nearly saturate the average credit card spending limit of $4,700, declaring an average balance of $3,800. Paycheck-to-paycheck consumers not struggling to pay their bills report an average spending of $3,100 and a limit of $6,500. Consumers not living paycheck to paycheck report an average spending of $2,100 and a $9,000 limit.Many paycheck-to-paycheck consumers remain creditworthy, maintain good credit scores, and are apt to tap into consumer loans, credit cards and other payment options such as personal loans to manage their cash flows.

“As the Fed looks to curb inflation by raising interest rates, consider looking at any credit you have with a variable interest rate,” continued Nayar. “Many of LendingClub’s 4 million members have already refinanced their variable interest rate credit card balance into a lower cost fixed rate loan so they can responsibly manage their debt obligations.”

Content created by Conservative Daily News and some content syndicated through CDN is available for re-publication without charge under the Creative Commons license. Visit our syndication page for details and requirements.

We desparately need a new POTUS!