Pending home sales fell slightly in August and have now decreased on an annual basis for eight straight months, according to the National Association of Realtors.

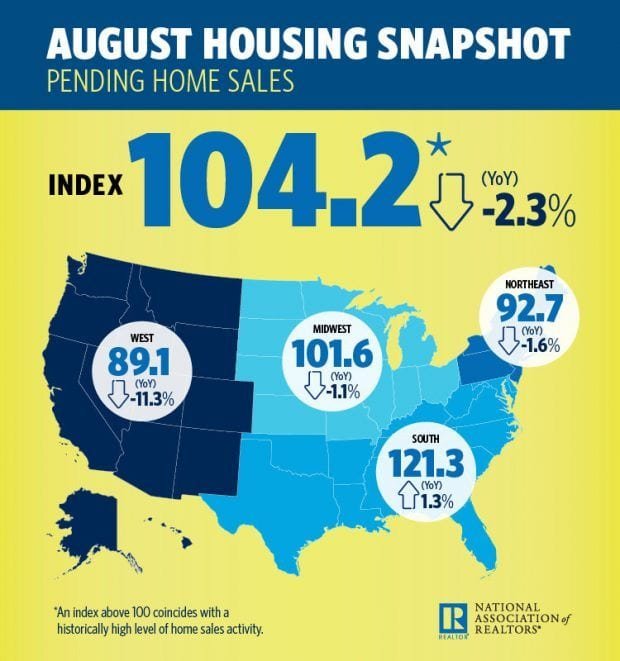

The Pending Home Sales Index, a forward-looking indicator based on contract signings, decreased 1.8 percent to 104.2 in August from 106.1 in July. With last month’s decline, contract signings are now down 2.3 percent year-over-year.

Lawrence Yun, NAR chief economist, says that low inventory continues to contribute to the housing market slowdown. “Pending home sales continued a slow drip downward, with the fourth month over month decline in the past five months,” he said.

Contract signings also fell backward again last month, as declines in the West negatively impacted overall activity,” he said. “The greatest decline occurred in the West region where prices have shot up significantly, which clearly indicates that affordability is hindering buyers and those affordability issues come from lack of inventory, particularly in moderate price points.”

According to the third quarter Housing Opportunities and Market Experience (HOME) survey, a record high number of Americans believe now is a good time to sell. “Just a couple of years ago about 55 percent of consumers indicated it was a good time to sell; that figure has climbed close to 77 percent today.”

Added Yun, “With prices having risen so quickly, many consumers were deciding to wait to list their homes hoping to see additional price and equity gains. However, with indications that buyers are beginning to pull out, price gains are going to decelerate and potential sellers are considering that now is a good time to list and bring more properties to the market.”

Yun pointed to year-over-year increases in active listings from data at realtor.com to illustrate a potential rise in inventory. Columbus, Ohio, Seattle–Tacoma–Bellevue, Wash., San Diego–Carlsbad, Calif., Providence–Warwick, RI-Mass. and Nashville, Tenn.saw the largest increase in active listings in August compared to a year ago.

When it comes to rising mortgage rates, Yun believes that while rising rates are always a deterrent to potential buyers, it should not lead to a significant decline. “We have two opposing factors affecting the market: the negative impact of rising mortgage rates and the positive impact of continued job creation. This should lead to future homes sales staying fairly neutral,” said Yun. “As long as there is job growth, rising mortgage rates will hinder some buyers; but job creation means second or third incomes being added to households which gives consumers the financial confidence to go out and make a home purchase.”

Yun expects existing-home sales this year to decrease 1.6 percent to 5.46 million, and the national median existing-home price to increase 4.8 percent. Looking ahead to next year, existing sales are forecast to rise 2 percent and home prices around 3.5 percent.

August Pending Home Sales Regional Breakdown

The PHSI in the Northeast dropped 1.3 percent to 92.7 in August, and is now 1.6 percent below a year ago. In the Midwest, the index slid back 0.5 percent to 101.6 in August and is also 1.1 percent lower than August 2017.

Pending home sales in the South dipped 0.7 percent to an index of 121.3 in August, however, it is 1.3 percent higher than a year ago. The index in the West decreased 5.9 percent in August to 89.1 and plummeted 11.3 percent below a year ago.

The National Association of Realtors® is America’s largest trade association, representing 1.3 million members involved in all aspects of the residential and commercial real estate industries.

*The Pending Home Sales Index is a leading indicator for the housing sector, based on pending sales of existing homes. A sale is listed as pending when the contract has been signed but the transaction has not closed, though the sale usually is finalized within one or two months of signing.

The index is based on a large national sample, typically representing about 20 percent of transactions for existing-home sales. In developing the model for the index, it was demonstrated that the level of monthly sales-contract activity parallels the level of closed existing-home sales in the following two months.

An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined. By coincidence, the volume of existing-home sales in 2001 fell within the range of 5.0 to 5.5 million, which is considered normal for the current U.S. population.